What is the source of the gap?

Recently, shares in new consumption stocks have experienced a significant pullback,$POP MART (09992.HK)$yet they continue to thrive.

Since August, Pop Mart’s stock price has increased by 37%, with a market capitalization exceeding 400 billion yuan.

Recently, Pop Mart’s mini version of LABUBU sold 300,000 units in just one minute.

Investors are observing, wondering who the next Pop Mart will be.

At present, the company that is closest to Pop Mart domestically is likely still$MINISO (MNSO.US)$。

However, in the past six months,$MNSO (09896.HK)$, there have been fluctuations and numerous setbacks.

In May of this year, when it announced its full-year performance for 2024, Miniso’s stock plummeted by 20% in a single day.

Following the recent release of Miniso’s performance for the first half of 2025, the stock surged over 20% in a single day.

Currently, Miniso’s market capitalization is still less than HKD 60 billion, with a valuation of only 22 times earnings, which has not garnered significant investor enthusiasm.

One Pop Mart is nearly equivalent to 7 to 8 Miniso stores.

Whether it is the gap between Miniso and Pop Mart, or the significant fluctuations in Miniso’s stock price following its two earnings reports, the root cause ultimately lies in the same issue—Intellectual Property (IP).

01

The point of divergence regarding Miniso’s stock price volatility lies in the market’s lingering doubts about whether Miniso can successfully reinvent its business model.

In the first half of 2025, Miniso achieved revenue of RMB 9.393 billion, representing a year-on-year increase of 21.1%. The net profit attributable to the parent company, after excluding non-recurring items, was RMB 919 million, a decline of nearly 20% year-on-year.

Despite such performance, the stock price can still surge, primarily due to Miniso’s impressive overseas business.

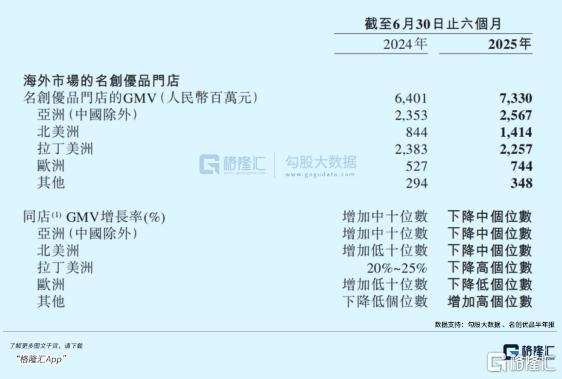

In the first half of 2025, Miniso opened 554 new stores in overseas markets, nearly three times the number of new stores opened in the mainland.

In the past year, nearly 75% of the new stores globally were opened overseas, making it a vital growth engine for Miniso.

It is evident that although it boasts two major brands, Miniso and TOPTOY, the company still primarily relies on store expansion in a retail store model to drive performance growth.

Under this model, Miniso’s performance growth is likely to hit a ceiling easily.

Moreover, due to the significant expansion of overseas stores, the costs associated with the direct operation model, including rent, labor, and complex supply chain management, have kept Miniso’s overseas operational costs high.

As the number of stores increases, the same-store GMV growth rate for Miniso’s overseas and mainland stores has even shown a ‘low single-digit’ negative growth.

And this is precisely the drawback of the retailer model.

While the franchise model can still earn profits through franchise fees and the procurement of franchisees, in the self-operated model, as the density of stores gradually increases, the competition among stores will intensify. The more stores there are, the less profitable each individual store becomes, which is almost self-evident.

It is also for this reason that Miniso’s retailer model is getting closer to its ceiling.

The market is watching whether Miniso can truly achieve a transformation of its business model and empower its stores through IP.

The potential of IP is immense.

In the first half of 2025, Pop Mart’s revenue reached 13.876 billion yuan, 1.5 times that of Miniso, with a year-on-year growth of 204.4%, approaching ten times that of Miniso.

Miniso’s gross margin in the first half of the year was 44.3%, a slight increase of 0.6 percentage points year-on-year, which is already quite remarkable, but Pop Mart’s gross margin during the same period reached 70.3%, an increase of 6.3 percentage points year-on-year.

Behind this is almost entirely the result of brand premium and IP operations.

In the first half of 2025, the revenue from Pop Mart’s own products accounted for as much as 99.1%, with revenue from artist IP accounting for 88.1%, and a total of 13 artist IPs generated over 100 million.

Also due to the strength of IP and brand, Pop Mart’s overseas expansion has been swift. In the first half of 2025, revenue from overseas regions exceeded 40%, and all regional markets achieved triple-digit growth.

Although Miniso is a latecomer in the IP economy, it is understandable that there is a gap compared to Pop Mart.

However, since starting its journey in the IP economy in 2016, Miniso has been deeply engaged in the IP economy for nearly 10 years.

Collaborations with IPs such as Sanrio and Harry Potter have also brought significant revenue to Miniso.

How far is Miniso from becoming the next Pop Mart?

02

The entire process of IP circulation can be divided into several stages: IP production, IP operation, product development, and product sales.

At the end of last year, when the Guzi economy launched the first shot of new consumption, several research reports classified Miniso and Pop Mart as part of the downstream of the IP industry chain, specifically the production and sales of IP derivatives.

However, today we can see that although Pop Mart is nominally a trendy toy retail store, in actual operations, Pop Mart is deeply involved in the entire process of IP circulation.

Whether it is externally sourced IP or internally produced IP, they are ultimately launched by the Pop Mart platform, and in the actual product design, Pop Mart also makes adjustments to the development of IP products; the currently popular LABUBU has undergone multiple version updates.

This year, Pop Mart’s revenue has already surpassed that of Japan’s Sanrio.

Therefore, the current distinction between Miniso and Pop Mart is essentially the difference between the upstream and downstream of the industry.

Similar to Pop Mart, after experiencing success from the collaboration with Sanrio on co-branded products in 2016, Miniso began to gradually source IP externally.

In the following years, Miniso gradually collaborated with over 150 globally renowned intellectual properties (IPs), including Barbie, Sanrio, Harry Potter, and Marvel, and was once referred to as the “IP wish pool,” from which Miniso profited significantly.$Disney (DIS.US)$In the following years, Miniso gradually collaborated with over 150 globally renowned intellectual properties (IPs), including Barbie, Sanrio, Harry Potter, and Marvel, and was once referred to as the “IP wish pool,” from which Miniso profited significantly.

Image source: Tuchong Creatives

However, sourcing IPs is a double-edged sword.

While developing popular IPs can ensure visibility, it means that manufacturers or enterprises on the sales end must endlessly pay upstream copyright holders to acquire licensed IPs, and then sell the products to downstream distributors to earn a share of the profits.

The profit margin from the price difference in the middle is quite limited, and there is little bargaining power among the contracted IPs.

In 2015, Pop Mart once introduced a Japanese IP, Sonny Angel, whose sales reached half of the company’s total annual sales at one point. However, at that time, the copyright holder of Sonny Angel decided to terminate the collaboration with Pop Mart, which dealt a significant blow to the company.

Moreover, even if an IP is popular, the sales and revenues after product development are equally uncertain.

Taking Miniso as an example, there was previously an expectation to create a hit product based on the Harry Potter IP; however, subsequent sales after development were disappointing.

However, for companies starting in IP development and sales, sourcing IP externally is an inevitable path.

Taking TOP TOY, a subsidiary of Miniso, as an example, initially, TOP TOY’s products were composed of 70% externally sourced IP and 30% original or co-created IP.

The founder and CEO of TOP TOY, Sun Yuanwen, summarized this model as follows—

Sourcing external IP can guarantee sales, but it comes with low gross profit margins and high inventory risks. Exclusive IP has high gross profit margins and is easier to cultivate fans from an emotional perspective, but the failure probability is also high; nurturing a successful original IP requires continuous trial and error.

Currently, TOP TOY’s self-operated products and externally sourced products are evenly split, and Sun Yuanwen stated that in the future, the ratio should be adjusted to 70-30.

At present, TOP TOY, a subsidiary of Miniso, has signed contracts with nearly 200 independent designers, including Japan’s top model prototype designer, Hiroshi Yokoyama, focusing on original IP research and development and collaboration.

From the results, last year, the original IP Nommi, which was exclusively signed by TOP TOY, generated over 100 million in revenue across all channels, with expectations of reaching 250 million this year and 500-600 million next year, indicating that it has already gained a certain level of recognition.

This year, TOPTOY also secured an investment led by Temasek, achieving a post-investment valuation of approximately HKD 10 billion.

In the future, Miniso and TOPTOY are bound to increase their investments in original intellectual property.

However, the more original and exclusive the intellectual property, the more it relies on operations and development.

The most significant characteristic of young consumers is their rapidly changing preferences; especially in the face of an explosion of original intellectual properties, how to manage and develop suitable products poses a challenge for Miniso.

Nevertheless, from another perspective, once the proprietary IP model is validated, Miniso, with its extensive network of stores worldwide, can quickly distribute products nationwide. Particularly, Miniso possesses operational experience across various products, providing it with a certain advantage in the development of IP derivative products.

At that time, Miniso’s IP and stores will be able to empower each other, yielding greater growth. Furthermore, the development of Chinese trendy toys overseas is already in a phase of rapid expansion.

During this stage, Miniso’s proprietary IP strategy can be explored gradually.

03

Conclusion

In a domestic environment where there is little room for further expansion, an increasing number of companies are shifting their focus to overseas markets.

From this perspective, Miniso has been quite successful, with overseas revenue accounting for nearly 40%, and this proportion continues to rise.

It is not difficult to see that compared to technology companies and other consumer goods companies, Miniso’s overseas expansion has been much smoother.

On one hand, this is due to Miniso’s operational capabilities; on the other hand, the underlying aspect of the IP economy is emotional consumption, which is further enhanced by cultural attributes.

Consequently, as Chinese culture gradually gains more recognition from foreigners, the related industries of the IP economy and emotional consumption are bound to flourish overseas. From this standpoint, the future development of Miniso and other related industries may still hold considerable potential.

However, before that, many changes need to be effectively implemented. (End of text)

Editor/joryn